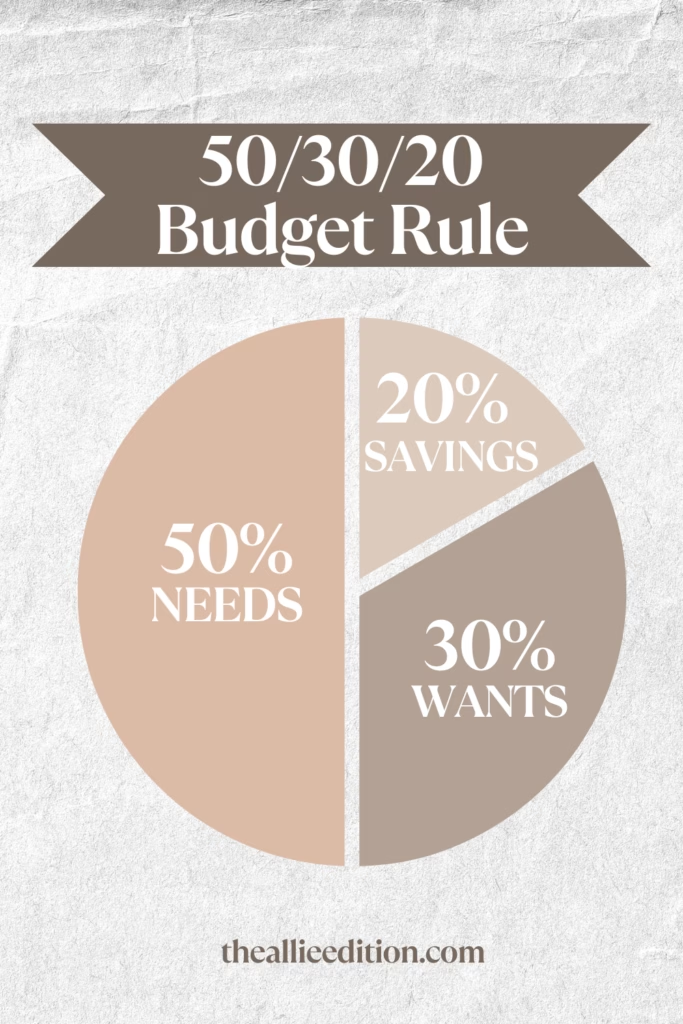

What is the 50 30 20 Budget Rule?

I’ve had a lot of people reach out to me asking how to get started with budgeting, so I decided to create a mini-series that breaks down three of the most basic budgeting methods out there. This includes the 50/30/20 budget rule, the 70/20/10 budget rule, and the zero-based budgeting method.

If budgeting feels overwhelming or you’re not sure where your money is actually going each month, stick around — this is completely normal. Most people aren’t looking for something complicated, just a simple starting point. And that’s exactly what this mini-series is meant to be.

This is the first post in the series, and it focuses on the 50/30/20 budget rule — what it means, how it works, and how you can apply it to your budget today.

Let’s get started.

This site contains affiliate links. These help fund my blog site at no extra cost to you. View the disclaimer for more information.

What is the 50 30 20 Budget Rule?

It’s actually really simple.

- 50% of your budget gets allocated to needs

- 30% of your budget gets allocated to wants

- 20% of your budget gets allocated to savings/debt

When you total this up, 100% of your budget should be fully allocated across these 3 budget categories.

What Do We Mean By “Needs, Wants and Savings/Debt” for the 50 30 20 Budget Rule?

Needs include things like…

- Rent/mortgage

- Utilities (gas, water, electric)

- Groceries, toiletries, or other essentials

- Insurance (car, health, home)

- Minimum debt payments

- Transportation (gas, tolls, parking)

If you are struggling to determine whether your expense is considered a need or a want, ask yourself, “Can you live without it? Are there impacts of not paying this expense (i.e. late fees, fines, etc.)?”

Wants include things like…

- Dining out, ordering food online, and entertainment

- Shopping and hobbies

- Subscriptions (Apple, Netflix, Spotify)

- Gym membership

- Vacation and travel

- Upgrades and luxuries

Think of this bucket like your nice-to-have’s. Sometimes these feel like needs, but in reality, they are not essential. They are just wants.

Savings & Debt includes things like…

- Personal sinking funds (vacation, gifts)

- Emergency fund

- Retirement contributions

- Extra debt payments (to pay off the principal)

- Investment accounts (Fidelity, Vanguard, Charles Schwab)

- Big purchases (house, car)

This is your opportunity to pay yourself first. When you get your paycheck, you should plan to allocate 20% here and can choose to spread it across 1 or more of the items I listed above. For example, you might choose to put 5% savings across 4 of these: sinking funds, emergency fund, retirement contributions, and debt payments.

Find Smart Tools to Budget Better, Save More, and Work From Anywhere

Ready to make life (and money management) a little easier? Check out my favorite tools, books, and essentials for budgeting smarter, building real savings, organizing your home office, and thriving in remote work—so you can create the flexible lifestyle you’re working toward.

How Can I Apply the 50 30 20 Budget Rule to My Finances?

Let’s play out this scenario using a salary of $45,000/year or $3,750/month (gross income, before taxes).

When we budget, we want to use net income (in other words, the amount of money that actually hits your bank account after taxes/fees are deducated). So now, let’s pretend that of the $3,750/month, your take-home pay is $3,400. We would utilize the 50 30 20 budget rule as follows:

Example for $3,400/month take-home pay

| 50% needs | $3,400 x 50% | $1,700 |

| 30% wants | $3,400 x 30% | $1,020 |

| 20% savings | $3,400 x 20% | $680 |

What If My Expenses Make Up More Than 50% of My Income?

It’s important to remember that personal finance is personal. Meaning, each person’s financial situation is going to look completely different. Therefore, you will require a budget unique to your income/expenses. If your expenses make up 60% of your income, you’ll simply want to adjust the other percentages for wants and savings.

For example, you could budget this way instead: 60% needs, 20% wants, 20% savings. For more information on how to start a budget, check out my beginner’s guide here.

How Do I Track My Budget Using the 50 30 20 Budget Rule?

I would highly recommend tracking your budget regularly, whether that be on a weekly or biweekly basis, to make sure you are staying within your budget for each category. There are several ways to do this:

- Download a personal finance app (my favorite is EveryDollar by Dave Ramsey)

- Get a physical budgeting planner (I like this one by Clever Fox)

- Explore digital budgeting spreadsheets (I use this one for my business)

- See if your banking apps offer budget tracking (if you bank with Chase, their app offers this!)

For more tips on how to track your finances consistently without getting burnt out or demotivated, check out this post.

Pros of the 50 30 20 Budget Rule

The best thing about this budgeting rule is that it is super simple to follow and even easier to remember. As compared to the zero-based budgeting method where you are assigning every single dollar a job, this rule allows you to simply track your spend against a broader category/amount. As long as you don’t go over, for example, 50% of your budget in needs, 30% of your budget in wants, and 20% of your budget in savings, then you are solid.

Not only that, but following the 50 30 20 budget rule helps you reinforce basic money management and gain a stronger sense of where your money is going each month.

Further, it suggests that you save 20% each month which is far more than most people tend to save. A good rule of thumb is to save at least 10-15% of your money toward retirement and following this rule enables you to do that, then an extra 5-10% toward other savings goals such as for vacation, a home, or a car.

Cons of the 50 30 20 Budget Rule

While the 50/30/20 budget rule can be a helpful starting point, it isn’t right for everyone.

As mentioned earlier, many people find that their expenses make up more than 50% of their income — and this is extremely common. When that’s the case, following the 50/30/20 rule exactly as structured can start to feel unrealistic.

Trying to force your spending into fixed percentages may lead to consistent overspending in certain categories, especially during seasons when expenses naturally fluctuate. Unexpected medical bills, higher utility costs, or holiday spending can all warrant changes in your spending patterns. Because this rule assumes your income and expenses will stay relatively consistent month to month, it doesn’t always leave room for real-life changes.

Over time, this can lead to burnout, overwhelm, or even a loss of confidence in your ability to manage your finances.

Is the 50 30 20 Budget Rule Right for You?

There is no “one right way” to budget.

The best budgeting method is the one that fits your lifestyle, reflects your real expenses, and helps you stay consistent. If the 50 30 20 budget rule gives you structure without feeling restrictive, it may be a great option. If it feels stressful or unrealistic, that’s a sign to explore a different approach.

As long as you understand how much money you’re working with and you’re consistently tracking where it’s going, you’re already setting yourself up for success.

What’s Next?

Check out my next post in this series where I break down the 70 20 10 budget rule.

Have any questions? Don’t hesitate to drop a comment below — I’d love to help.