What is the 70 20 10 Budget Rule?

I’ve had a lot of people reach out to me asking how to get started with budgeting, so I decided to create a mini-series that breaks down three of the most basic budgeting methods out there. This includes the 50/30/20 budget rule, the 70/20/10 budget rule, and the zero-based budgeting method.

If budgeting feels overwhelming or you’re not sure where your money is actually going each month, stick around — this is completely normal. Most people aren’t looking for something complicated, just a simple starting point. And that’s exactly what this mini-series is meant to be.

This is the second post in the series, and it focuses on the 70 20 10 budget rule — what it means, how it works, and how you can apply it to your budget today.

Let’s get started.

This site contains affiliate links. These help fund my blog site at no extra cost to you. View the disclaimer for more information.

What is the 70 20 10 Budget Rule?

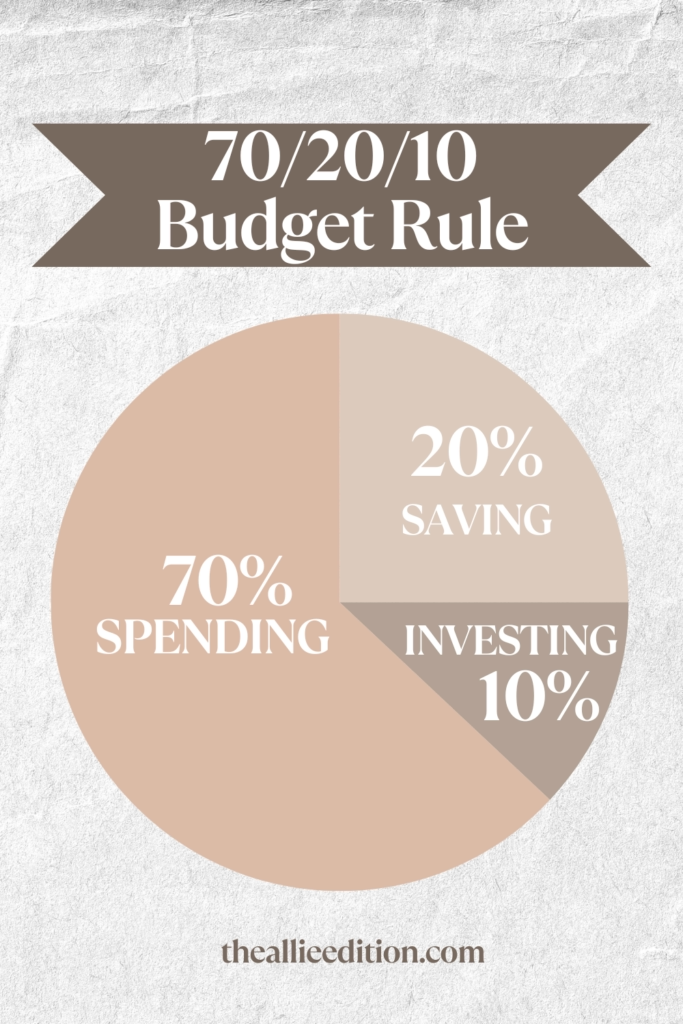

This method divides your money in 3 simple ways:

- 70% of your budget gets allocated to spending

- 20% of your budget gets allocated to saving (or debt)

- 10% of your budget gets allocated to investing (or giving)

When you total this up, 100% of your budget should be fully allocated across these 3 budget categories.

What Do We Mean By “Spending, Saving, and Investing” for the 70 20 10 Budget Rule?

The spending category encompasses all living expenses, both needs and wants, like…

- Rent/mortgage

- Utilities

- Transportation (gas, tolls, parking)

- Insurance

- Groceries/Toiletries

- Minimum debt payments

- Restaurants

- Shopping

- Hobbies

- Subscriptions (Apple, Netflix, Spotify)

- Childcare

- Pets

- Vacation/Travel

The saving category can span a set of savings goals or debt payoff goals like…

- Personal sinking funds

- Emergency fund

- Retirement contributions

- Extradebt payments (to pay off the principal)

- Big purchases (house, car)

This is your opportunity to pay yourself first. When you get your paycheck, you should plan to allocate 20% here and can choose to spread it across 1 or more of the items I listed above. For example, you might choose to put 5% savings across 4 of these: sinking funds, emergency fund, retirement contributions, and debt payments.

The final category is for investing (or giving) for things like…

- Stocks or bonds

- ETFs or mutual funds

- Cryptocurrency

- Real estate

- Business start-up

- Charity and donations

If you are new to investing, I would start by checking out Fidelity, Vanguard, and Charles Schwab. I have tried all 3 before but I personally choose to stick with Fidelity. Here, I have an individual brokerage account where I invest in a variety of stocks, bonds, ETFs, and mutual funds. Fidelity is super easy and beginner-friendly to use, I highly recommend it!

Find Smart Tools to Budget Better, Save More, and Work From Anywhere

Ready to make life (and money management) a little easier? Check out my favorite tools, books, and essentials for budgeting smarter, building real savings, organizing your home office, and thriving in remote work—so you can create the flexible lifestyle you’re working toward.

How Can I Apply the 70 20 10 Budget Rule to My Finances?

Let’s play out this scenario using a salary of $45,000/year or $3,750/month (gross income, before taxes).

When we budget, we want to use net income (in other words, the amount of money that actually hits your bank account after taxes/fees are deducated). So now, let’s pretend that of the $3,750/month, your take-home pay is $3,400. We would utilize the 50 30 20 budget rule as follows:

Example for $3,400/month take-home pay

| 70% spending | $3,400 x 70% | $2,380 |

| 20% saving | $3,400 x 20% | $680 |

| 10% investing | $3,400 x 10% | $340 |

What If My Personal Finance Goal(s) Require Me To Save More Than 20%?

It’s important to remember that personal finance is personal. Meaning, each person’s financial situation is going to look completely different. Therefore, you will require a budget unique to your income/expenses. If your personal finance goals require you to save more than 20% a month (or invest more than 10%) then you simply would want to adjust the weighted percentage across each of the 3 categories.

For example, you could budget this way instead: 60% spending, 30% saving, 10% investing. For more information on how to start a budget, check out my beginner’s guide here.

How Do I Track My Budget Using the 70 20 10 Budget Rule?

I would highly recommend tracking your budget regularly, whether that be on a weekly or biweekly basis, to make sure you are staying within your budget for each category. There are several ways to do this:

- Download a personal finance app (my favorite is EveryDollar by Dave Ramsey)

- Get a physical budgeting planner (I like this one by Clever Fox)

- Explore digital budgeting spreadsheets (I use this one for my business)

- See if your banking apps offer budget tracking (if you bank with Chase, their app offers this!)

For more tips on how to track your finances consistently without getting burnt out or demotivated, check out this post.

Pros of the 70 20 10 Budget Rule

Similarly to the 50 30 20 budget rule, this gives you a simple structure to follow making it easy for beginners to follow. This budget rule, too, helps you reinforce basic money management and gain a stronger sense of where your money is going each month.

I personally love the 70 20 10 budget rule because it encourages a more aggressive saving and investing ratio, helping people to get out of debt and save more money. This is perfect for those who are getting introduced to saving and investing at a later stage in life and are trying to fast track their way to their finance goals (such as building a 6-12 month emergency fund, paying off your home, building an investment portfolio or retiring).

Lastly, this rule is great because it allows more flexibility when it comes to your needs and wants. As compared to the 50 30 20 budget rule, where some may find difficulty containing their living expenses to 50% of their income, this rule allows you to stretch it as much as 70%.

On that note though, if 70% if your income is solely needs (like bills and debt payments) as opposed to a healthy balance of needs and wants, then I highly recommend looking at ways to increase sources of income so you can lower this percentage to 50% or less.

Cons of the 70 20 10 Budget Rule

While the 70 20 10 budget rule can be a helpful starting point, it isn’t right for everyone.

There are some people who will require more than 20% monthly saving or 10% monthly investing ratios in order to hit their finance goals (maybe age and timing plays a factor here). On the flip side, others will have difficulty saving/investing as much as 30% of their income.

For me, personally, I struggle with this rule because it does not allow you to separate your needs from your wants. I like to see these broken into sub categories so I can closely track how much of my budget is going toward bills versus leisure spending. If that sounds like you too, you may wish to explore other budgeting methods like zero-based budgeting.

Is the 70 20 10 Budget Rule Right for You?

There is no “one right way” to budget.

The best budgeting method is the one that fits your lifestyle, reflects your real expenses, and helps you stay consistent. If the 70 20 10 budget rule gives you structure without feeling restrictive, it may be a great option. If it feels stressful or unrealistic, that’s a sign to explore a different approach.

As long as you understand how much money you’re working with and you’re consistently tracking where it’s going, you’re already setting yourself up for success.

What’s Next?

Check out my next post in this series where I break down zero-based budgeting.

Have any questions? Don’t hesitate to drop a comment below — I’d love to help.