What is Zero-Based Budgeting (Example Included)?

I’ve had a lot of people reach out to me asking how to get started with budgeting, so I decided to create a mini-series that breaks down three of the most basic budgeting methods out there. This includes the 50/30/20 budget rule, the 70/20/10 budget rule, and the zero-based budgeting method.

If budgeting feels overwhelming or you’re not sure where your money is actually going each month, stick around — this is completely normal. Most people aren’t looking for something complicated, just a simple starting point. And that’s exactly what this mini-series is meant to be.

This is the third post in the series, and it focuses on the zero-based budgeting method— what it means, how it works, and how you can apply it to your budget today.

Let’s get started.

This site contains affiliate links. These help fund my blog site at no extra cost to you. View the disclaimer for more information.

What is the Zero-Based Budgeting Method?

This is not only my favorite budgeting method, but it is the best method for those who are trying to gain ultimate control over their money. This method helps you see exactly where your money is coming and going.

Put simply, every dollar you earn is assigned a job, whether that be for spending, saving, investing, donating, or paying off debt. Every single dollar should be accounted for so that if you subtract your expenses from your income, you end up with $0.

In this post, I’ll share some examples of budget categories you can assign your dollars to, followed by how this compares to other methods such as the 50/30/20 budget rule and the 70/20/10 budget rule, and finally a zero-based budget example that you can use to start budgeting today.

What Spending Categories Should I Use for the Zero-Based Budgeting Method?

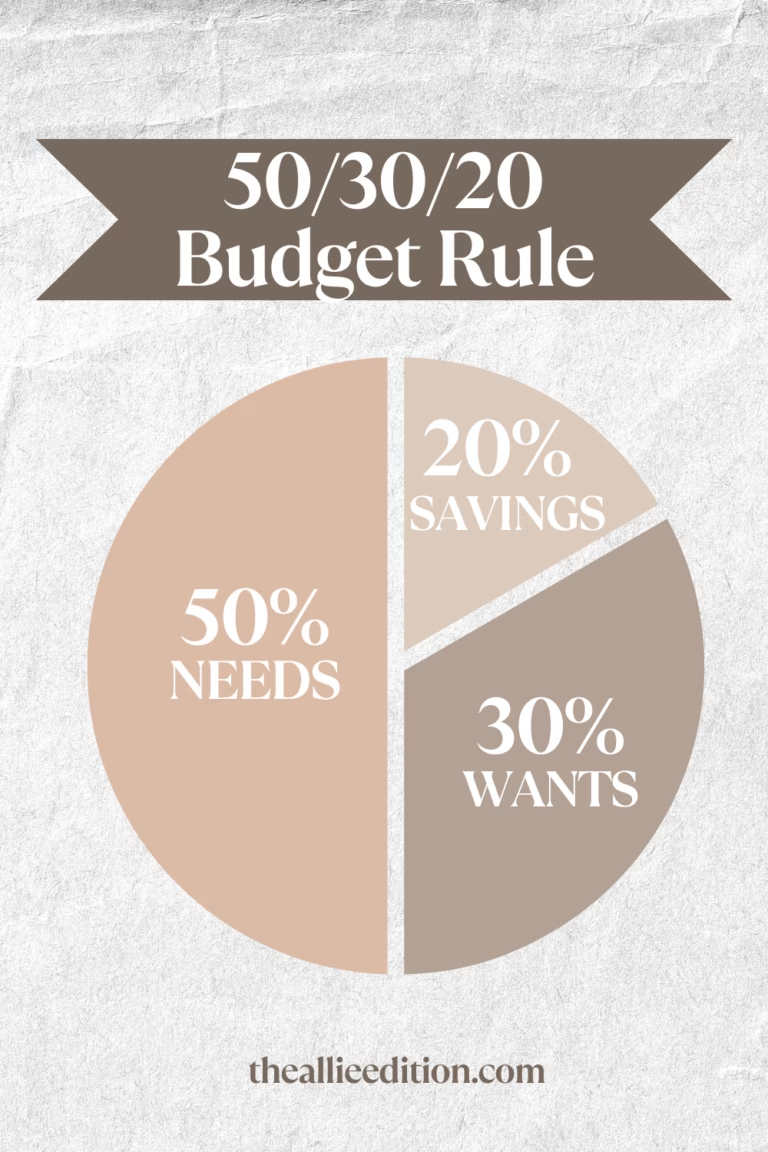

Let’s start by thinking about where you might assign your money. There are three broad categories that come to mind, which if you’ve already read about the 50/30/20 budget rule, these will sound familiar: needs, wants and saving.

From there, I would break each broader category into subcategories, which is how you will truly allocate your budget. Here is a breakdown of those subcategories by needs, wants and saving:

Needs include things like…

- Rent/mortgage

- Utilities (gas, water, electric)

- Groceries, toiletries, or other essentials

- Insurance (car, health, home)

- Minimum debt payments

- Transportation (gas, tolls, parking)

If you are struggling to determine whether your expense is considered a need or a want, ask yourself, “Can you live without it? Are there impacts of not paying this expense (i.e. late fees, fines, etc.)?”

Wants include things like…

- Dining out, ordering food online, and entertainment

- Shopping and hobbies

- Subscriptions (Apple, Netflix, Spotify)

- Gym membership

- Vacation and travel

- Upgrades and luxuries

Think of this bucket like your nice-to-have’s.

Savings & Debt includes things like…

- Personal sinking funds (vacation, gifts)

- Emergency fund

- Retirement contributions

- Extra debt payments (to pay off the principal)

- Investment accounts (Fidelity, Vanguard, Charles Schwab)

- Big purchases (house, car)

This is your opportunity to pay yourself first. I personally aim to make sure at least 15% of my budget goes toward savings/debt, with the ultimate goal being 30%. Of this amount, I try to put at least 5-10% toward investing in retirement. Note: this is only for educational purposes, this is not financial advice.

Find Smart Tools to Budget Better, Save More, and Work From Anywhere

Ready to make life (and money management) a little easier? Check out my favorite tools, books, and essentials for budgeting smarter, building real savings, organizing your home office, and thriving in remote work—so you can create the flexible lifestyle you’re working toward.

Zero-Based Budget Example

Alright, let’s look at an example of the zero based budget in action. In this example, we’ll be using a salary of $45,000/year or $3,750/month (gross income, before taxes).

When we budget, we want to use net income (in other words, the amount of money that actually hits your bank account after taxes/fees are deducated). So now, let’s pretend that of the $3,750/month, your take-home pay is $3,400. We would utilize the 50 30 20 budget rule as follows:

Zero-Based Budget Example for $3,400/month take-home pay

| Rent | $1,500 |

| Utilities | $200 |

| Insurance | $125 |

| Groceries | $300 |

| Transportation | $100 |

| Min. Debt Payment | $225 |

| Dining/Takeout/Entertainment | $120 |

| Shopping | $100 |

| Subscriptions | $30 |

| Gym Membership | $10 |

| Personal sinking funds (vacation, gifts) | $150 |

| Emergency fund | $100 |

| Retirement contributions | $340 |

| Extra debt payments | $50 |

| Investment accounts (Fidelity, Vanguard, Charles Schwab) | $50 |

| TOTAL | $3,400 |

If I had $3,400 a month, this is how I would budget my money. This ensures that I am paying no more than 50% of my monthly income to afford rent/utilities. Further, it ensures that at least 10% of my income goes toward retirement, with at least 5% more going toward savings.

You will need to tailor your budget to your lifestyle and financial situation, but feel free to use this zero-based budget example as a starting point. Plug-in your actual monthly income, adjust the budget categories as needed, and start breaking down your budget for the month.

How Do I Track My Zero-Based Budget?

I would highly recommend tracking your budget regularly, whether that be on a weekly or biweekly basis, to make sure you are staying within your budget for each category. A simple way to track a zero-based budget is to spend approximately 10-15 minutes each week logging all of your expenses and comparing actual spend against the planned amount.

There are several ways to do this:

- Download a personal finance app (my favorite is EveryDollar by Dave Ramsey and it is literally designed for this method. Plus, it’s free!)

- Get a physical budgeting planner (I like this one by Clever Fox)

- Explore digital budgeting spreadsheets (I use this one for my business)

- See if your banking apps offer budget tracking (if you bank with Chase, their app offers this!)

For more tips on how to track your finances consistently without getting burnt out or demotivated, check out this post.

Pros of Zero-Based Budgeting

Zero-based budgeting is a great way to see exactly where your money is coming and going. If you are struggling to identify spending patterns in order to effectively cut back on costs, this budgeting method is the perfect solution.

Further, it gives you complete control to decide exactly how much money you will save and invest each month. This budgeting method is, in my opinion, the most realistic because each person has a unique financial situation, requiring that they allocate their income differently than the next person. Not only that, but if you consider holidays, anniversaries, etc., these times of the year also warrant unique spending and saving patterns.

Using the zero-based budgeting method means you have flexibility to accommodate these fluctuations in spending and saving. And not just for this month, but for every month. Want to save $100 this month, then $200 next month? No problem. Want to cut back more aggressively for 3 months so you can finally pay off that credit card? No problem. You are the boss.

Cons of Zero-Based Budgeting

As much as this budgeting method is my favorite, it’s not for everyone. Here’s why.

This particular budgeting method can feel more time consuming compared to other budgeting methods given it requires that you log each individual expense. Some people may feel like they do not have enough time to dedicate to this method or will find it overwhelming to start.

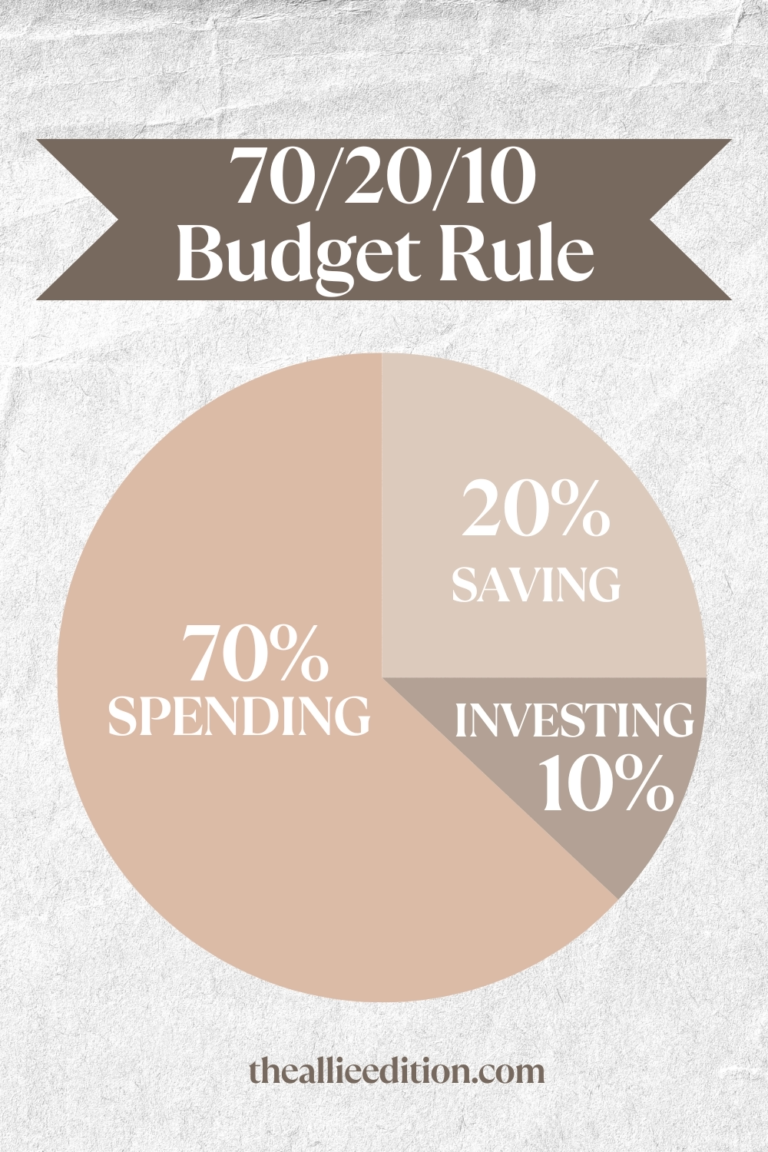

If this sounds like you, it may be best to try out more simple methods like the 50/30/20 budget rule or the 70/20/10 budget rule. As a reminder, any budget method can (and should) be tailored to suit your needs.

Is Zero-Based Budgeting Right for You?

There is no “one size fits all” when it comes to budgeting BUT,… If you are new to budgeting and are finally ready to gain control over your finances so you can hit your financial goals by the end of the year, this budgeting method may be perfect for you.

This is honestly my favorite budgeting method because I am a bit of a control-freak when it comes to my finances and I like to make sure that if I say I am going to save $5,000 this year for vacation, I have an exact plan in place to do so. And when I say having a plan in place, I mean having a solid budget.

If you have any questions, don’t hesitate to drop a comment down below. I’d love to help!

For more information on how to start a budget from scratch, check out my beginner’s guide here.