How to Build an Emergency Fund: Your Guide to Financial Security

Building an emergency fund is one of the most important steps in achieving financial security. But the question around how to build an emergency fund is something many people struggle with.

Whether you’re ready to get serious about building one, or you keep hearing about it and wondering what it really means for you, you’re in the right place.

I’m here to break it all down—why you need it, common questions on getting started, and more importantly, how to actually build one.

Time to say goodbye to stressing over life’s unexpected challenges and hello to an emergency fund that supports your lifestyle. Let’s get started.

This site contains affiliate links, view the disclaimer for more information.

Welcome to part 8 of 10 in my personal finance blog series, where we dive into how a money saving plan can be your key to successfully transitioning from debt to savings. If you’re just joining us, be sure to check out the first post for a deeper dive into why a money saving plan is so crucial. It’ll lay the foundation for everything we’re discussing moving forward.

Your Guide to Building an Emergency Fund

Why an Emergency Fund Is Important

An emergency fund is important because it gives you a financial cushion for whatever unexpected events life wants to throw your way. Having an emergency fund means, instead of saying, “How am I going to get through this?” you can confidently say, “This isn’t ideal, but I’m prepared.”

Think about it like this: You set aside $500 each month to pay off debt, and for the past 3 months, you’ve been on track with your budget. But then, out of nowhere, flat tire. Now, you need to come up with an extra $200 to pay that bill. Where’s that money going to come from? Your budget only allows you to put $500 toward debt, which means your whole debt repayment plan is thrown off track. But, if you had an emergency fund, you could easily pull from it and pay the $200 car bill without stressing. Why? Because you were financially prepared for the unexpected.

But hey, it’s not just about avoiding setbacks. Because if you’re working remotely—or juggling a freelance or side hustle schedule—there’s an extra layer of importance here. With remote work comes unpredictable income. An emergency fund means less financial “scares” and instead more financial stability when things get out of hand.

Not to mention, let’s talk about the freedom it gives you. When you’re not constantly stressing over surprise expenses, you can stay focused on your goals—whether that’s building savings, launching a blog, or finally upgrading your home office setup. And if you want to do something a little more bold—like investing in a course or taking time off to travel—you’ve got the flexibility to do it without impacting your finances.

Long story short: it’s not just about surviving emergencies. It’s about setting yourself up to thrive in spite of them.

Don’t forget to pin this!

Make sure to pin this to your Pinterest board so you can easily come back to these strategic tips on how to build an emergency fund.

How an Emergency Fund Fits into the Bigger Picture of a Money Saving Plan

When it comes to saving money, there’s a million and one things you can save for—car, home, vacation, education, etc. The one thing, though, that never fails is having an emergency fund to carry you when life gets out of hand. There’s no worse feeling than being stuck in a financial rut and thinking, “How on Earth am I going to get out of this one?”

Now, we can’t always be 100% prepared financially. But, if we can at least be a little prepared and have some financial cushion, that’s the goal.

It took me several years to build up my emergency fund, and full transparency, I’m still actively working on saving and maintaining it. Why? Because life happens. I had over $2k worth of unexpected vet bills when I adopted one of my cats. But guess where that money came from? My emergency fund. And guess what happened next? I worked on adding that $2k back to my emergency fund. Because maintaining your emergency fund is just as important as building it.

Give yourself a minimum threshold, and be sure to replenish your fund any time you dip into it (for actual emergencies, not for a “crisis” involving ice cream or late-night shopping sprees—sorry, ladies, I wish it worked that way).

How Much Do I Need in My Emergency Fund?

One of the most common questions people ask as they are learning how to build an emergency fund is: “So, how much do I need to save?”

Many financial experts recommend saving enough to cover 3-6 months of living expenses. For example, if you earn $40,000 per year, your emergency fund target would be calculated like this:

$40,000 ÷ 12 months = $3,333.33/month

$3,333.33 x 3 months = $10,000 total (minimum goal)

$3,333.33 x 6 months = $20,000 total (ideal)

Now let’s look at it this way: If you something were to come up tomorrow—whether it’s medical bills, funeral costs, you get laid off, or something like your car getting totaled—how much time would you need to get back on your feet?

The reality is, unexpected costs can hit at any time. That’s why I recommend a 6-month cushion if you can swing it. But just get started, and adjust as you go. Yes, this still applies if you can only get started with let’s say $5, 10, $25. Money adds up!

How Fast Do I Need to Build My Emergency Fund?

When learning how to build an emergency fund, another common question that tends to come up is, “How fast do I need to build it?”

The simple answer? Build it before you will need it.

There’s no way to predict exactly when something will go wrong, but sometimes the warning signs are there. Is illness going around? Are family members getting older? Are layoffs happening at your job? These are all reminders that now is the time to prepare. And the best way to protect yourself financially is by having money set aside to help you get through it.

So, when should you start building your emergency fund?

Right now. Don’t wait.

If you can build your emergency fund up fast, that’s fantastic. But don’t stress if you’re not able to hit your goal after just a few months. Everyone’s financial journey is different, so it’s important to be realistic.

The key is consistency. Each month, ask yourself: Am I saving as much as I can? Are there financial habits holding me back? Be honest. Be kind to yourself. And if you have an off month, give yourself grace. Come back to your “why” and keep going.

Can I Still Save for My Emergency Fund If I Have Debt?

Finally, if you’re interested in learning how to build an emergency fund while juggling debt, you might be wondering “Can I still save for my emergency fund if I have debt?”

Yes, yes, and yes! You absolutely can and should save while paying off debt. Why? Because having a safety net helps you avoid going deeper into debt when life hits you with unexpected costs. This doesn’t mean stop paying for debt entirely; it means finding a balance between saving and paying debt.

Consider your financial situation and create a ratio that works for you. For example, let’s say you can afford $1,000 a month for savings and debt payments. You might decide to allocate $500 to your emergency fund and $500 to pay down debt. If you’re dealing with high-interest debt (like credit card debt), consider dedicating more to pay it off first. Once that’s cleared, shift your focus to ramping up your emergency fund while still paying off your low-interest debt.

Your budget should be flexible and adapt with you as life goes on and your financial situation evolves. So don’t worry if things need to shift around. Just keep working towards a balance that feels sustainable.

10 Steps to Start Building an Emergency Fund

Alright, now that we’ve covered the big questions—why you need an emergency fund, how much to save, and how to balance it with debt—I hope you’re feeling more confident about taking action. If you still have questions, feel free to drop them in the comments below—I’m always happy to help!Now for the fun stuff: how to build an emergency fund step-by-step. Let’s break it down into simple, doable actions so you can start making real progress today.

1. Assess your financial situation

If you’re coming from my blog series, then you’ve heard me say this a few times before—but it truly is a key step for any and all financial planning.

This step is all about reviewing your finances and figuring out how much you can reasonably afford to put aside each month for your e-fund. Think about all your recurring expenses—monthly, quarterly, or even annual. Maybe you pay car insurance every month, get an oil change every three, and replace your windshield wipers once a year. Include essentials like bills, groceries, and toiletries—and yes, your “fun stuff” too: dessert runs, coffee habits, gum addictions… we’re being honest here, right?

2. Set a Clear Budget with Goals

I’ve said this before and I’ll say it again: set a budget with clear savings goals. It’s one of the best ways to build an emergency fund without burning out halfway through.

Start by setting some realistic milestones based on where you’re at in your financial journey:

- Short-term goal: Aim to save your first $1,000 as quickly as you can. Most people in the U.S. aren’t prepared for an unexpected $1,000 expense—don’t let that be you. Emergencies like a surprise car repair, a dental bill, or a last-minute flight to visit family can easily hit that amount. Be ready.

- Mid-term goal: Once you’ve got $1,000 set aside, focus on paying off any high-interest credit card debt. Then, start ramping up your emergency savings to cover 1–2 months of expenses. This gives you more cushion and helps you avoid falling back into debt if something unexpected happens.

- Long-term goal: Ultimately, work your way toward a fully funded emergency fund—ideally 3 to 6 months’ worth of essential expenses. It won’t happen overnight, but with consistent effort, you’ll get there.

Didaey store

Colorful, Fun Goal Charts

Let’s be real—watching your savings grow is way more fun when you can see your progress. These colorful thermometer goal charts are the perfect way to stay motivated while you build your emergency fund.

Use the SMART goal strategy to keep things realistic and trackable. For example: “Increase my emergency fund savings by $12,000 in 12 months.” Boom. Simple, specific, measurable.

Now break that down into bite-sized goals—like $1,000 per month or $500 per paycheck if you’re paid biweekly—so you can track your progress and celebrate those small wins.

3. Download a Budgeting App or Grab a Notebook

Whether you’re Team Digital or Team Pen-and-Paper, pick a system to track your budget and savings progress. Budgeting apps like EveryDollar by Dave Ramsey or planners like the Clever Fox Pro are both solid options to help visualize your goals, income, and expenses each month.

This isn’t just about “knowing where your money goes.” It’s about watching that emergency fund grow, week by week, until it’s right where you need it.

Clever Fox

Budget Planner

A simple, hands-on budget planner like this one can make it much easier to keep track of personal finances without letting anything slip through the cracks. No more accidental over-spending or expenses sneaking up on you.

4. Open a Savings Account (Premium or HYSA*)

This is a biggie.

If you don’t already have a savings account, it’s time to open one. The type you choose will depend on how much money you have ready to deposit.

Some banks offer premium savings accounts that pay you higher dividends just for keeping money in there. (Yes, actual free money.) Even better? If you qualify, go for a HYSA—a High-Yield Savings Account—which offers even higher interest rates.

I went from earning just $7/month in interest to over $80/month when I switched to a HYSA. That’s nearly $1,000/year just for letting my money sit there. No extra work, no stress.

Not eligible yet? No worries. Ask your bank about the minimum threshold and make that your next savings milestone.

P.S. Different banks offer different interest rates for their HYSA’s. I would recommend “shopping around” so you can make your money work harder for you and maximize total savings.

Find Smart Tools to Budget Better, Save More, and Work From Anywhere

Ready to make life (and money management) a little easier? Check out my favorite tools, books, and essentials for budgeting smarter, building real savings, organizing your home office, and thriving in remote work—so you can create the flexible lifestyle you’re working toward.

5. Automate Your Savings

Wherever possible, automate your finances. This makes money far less stressful and frees up time for you to focus energy on other important priorities in your life. If you have direct deposit setup for your paychecks, you can automate a percent or fixed dollar amount each month straight to your savings account. Just like you do for a 401k or loans.

Now, if you’re not super comfortable with this method–maybe because you’re not saving the same amount month-to-month or you would rather move the money yourself, I hear you. Here’s what I would do instead (although it requires more discipline). Each time you get your paycheck, immediately move out any funds directly to your savings account as if it were a bill payment (but this time, you’re paying yourself). This is a good way to make sure that the money is already out of your checking account before you start any personal spending and will help reduce the overall risk for overspending.

6. Cut Back on Unnecessary Expenses

Hold up—I’m not saying cut every little thing you enjoy out of your life. That’s not realistic and definitely not sustainable. Matter of fact, if someone told me to do that, I’d quit before I even got started.

What I am saying is take an honest look at your spending and see where you can scale back without making yourself miserable. A few ideas:

- Cancel unused subscriptions. (Do you really need five streaming platforms?)

- Reduce everyday habits. (Maybe limit coffee runs to 3x a week instead of daily.)

- Delay impulse buys. (Try a 48-hour pause rule—you might just forget about it.)

The goal is progress, not perfection.

7. Start a Money Saving Challenge

Saving doesn’t have to be boring. Try a money saving challenge to kick things off!

Start a swear jar, round-up spare change, or funnel all your “extra money” into your emergency fund—things like cash gifts, bonuses, tax refunds, or side hustle income. For more fun ideas, check out my full list of money saving challenges here.

This is a creative way to save without overthinking every dollar.

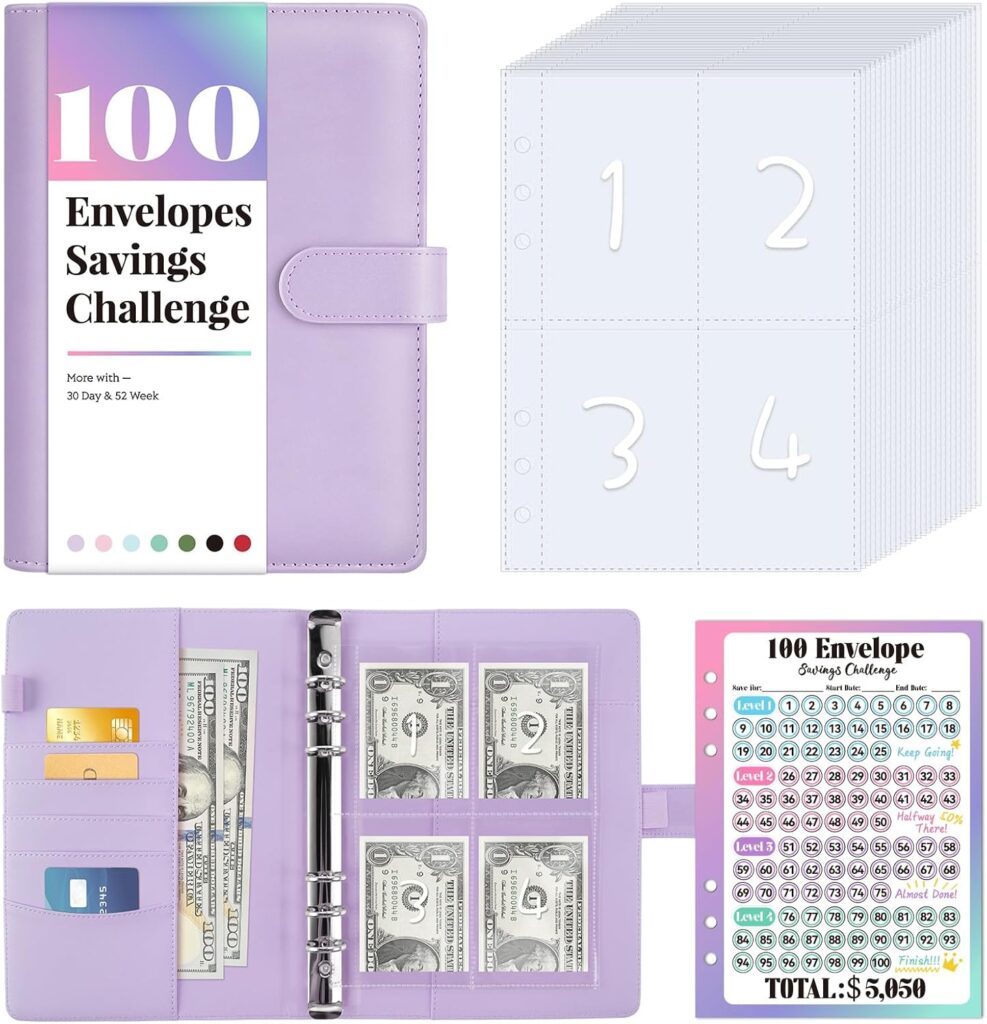

Sooez store

100 Envelopes Money Saving Challenge

Want to start saving but struggle to stay motivated? The 100 Envelopes Challenge is a fun and easy way to turn saving into a game.

- Set your savings goal and write it on the tracker.

- Pick an envelope and save the amount that matches the number on it.

- Cross it off the tracker as you go!

By the time you’ve marked off every number, you’ll have hit your goal—and built some serious momentum with your savings.

8. Find New Income Streams

At some point, cutting expenses just isn’t enough—and that’s your cue to find ways to bring in extra money.

You don’t need a second job (unless that’s your thing). There are tons of small, flexible ways to boost your income—many of which take little effort upfront:

- Sell stuff around your house: clothes, furniture, things you don’t use or that just collect dust. You’d be surprised how quick and easy it is to sell your “donation pile” on platforms like Facebook Marketplace (P.S it’s free!).

- Recycle things like bottles and cans. You’d be surprised how quickly that adds up.

- Offer services in your neighborhood or online—pet-sitting, baby-sitting, house-cleaning, virtual assistance, resume writing, you name it.

- Pick up overtime or holiday shifts if your job offers them.

- Monetize a hobby like baking, crafting, freeze-dried candy (yes, it’s a thing), or 3D printing.

Or hey—start a blog! It’s more than a creative outlet—it could be your first step toward financial freedom, flexibility, and something truly yours.

How I Turned My Hobby Into a Side Hustle

For years, I dabbled in different side hustles, but nothing felt like the right fit—until I discovered blogging. I wanted something profitable, flexible, and enjoyable, but I had no clue where to start. After weeks of researching blogging courses, I finally found Sophia Lee’s Beginner’s Blogging Bundle, and it changed everything.

This bundle includes two courses: Perfecting Blogging and Perfecting Pinterest. Perfecting Blogging breaks down SEO strategies, Sophia’s step-by-step formula for creating high-quality blogs fast, and the exact strategies she used to grow her site into a six-figure business. Perfecting Pinterest reveals her traffic-driving secrets, time-saving content strategies, and how to maximize Pinterest for rapid blog growth.

If you’re just starting out or struggling to get traction, this bundle gives you a clear roadmap to success. I can confidently say it made my blogging journey 100x easier, and I know it can do the same for you!

9. Monthly Progress Review

This step is key to staying motivated (and not accidentally going off track).

Set a reminder to review your budget and savings progress at least once a month. Look at:

- How much you’ve saved so far

- What’s working and what’s not

- Any upcoming expenses that might change your saving strategy

Be honest with yourself. Adjust your budget as needed and celebrate the wins—big or small.

Not seeing progress? Don’t give up. You might just need to revisit your timeline or shift your saving strategy (like increasing your income instead of cutting more corners). It’s easy to feel stuck when growth feels slow—but checking in helps you see the full picture, not just the tough moments.

Sometimes the biggest accomplishment is simply showing up and staying consistent—and that’s exactly what monthly check-ins help you do.

10. Don’t Dip Into Your Emergency Fund

Repeat after me: “I will not touch my emergency fund unless it’s truly an emergency.”

So what counts? Sudden medical bills, car repairs, home repairs, job loss, or urgent family matters. Not Sunday brunch with the girls. Not concert tickets because your favorite artist just dropped a tour in your hometown. And not a flash sale you just found out about.

If you need a money pot to pull from for miscellaneous spending, set up either a sinking fund or a separate personal savings account strictly for non-essentials. That way, you’ve still got something to dip into when life (or your mood) demands a little treat—but you’re not putting your future self at risk.

Personally, I keep three accounts:

- A checking account for bills and everyday spending

- A personal savings account that acts as a sinking fund for fun purchases, gifts, or future goals

- A HYSA (High-Yield Savings Account) that’s strictly for emergencies—hands off, no exceptions

Some people like to go a step further and open a fourth account just for bills or fixed expenses. That can be super helpful if you want ultra-clear organization. Whatever works best for your brain, your budget, and your lifestyle—get it set up and stick to a routine.

Start by paying your needs first (bills and savings), then your wants second. That shift alone can seriously change your money mindset—and help you build your emergency fund faster.

Any Questions?

Building an emergency fund is one of the most empowering things you can do for your financial future. It’s not just about saving; it’s about creating peace of mind, flexibility, and the ability to take bold steps toward your goals—whether that’s tackling debt, investing in yourself, or pursuing a new opportunity.

Now that you know exactly how to build an emergency fund, it’s time to take action. No matter where you are in your financial journey, it’s important that you get started today. Let’s make sure that when life throws those unexpected challenges your way, you’re ready for them. Start small, stay consistent, and celebrate every milestone along the way!

Drop a comment below if you have any questions or share your emergency fund journey—I’d love to hear from you!

Next up in the blog series

In Part 9 of this blog series, we’ll go more in-depth on how to identify and cut back on unnecessary expenses to further boost your savings!